Sampling from Distributions, Bar Plots, Histograms and Scatter plots#

Import and Settings#

We will import NumPy and matplotlib. In addition, we will also start with some customised layout for the plot.

import numpy as np

import matplotlib.pyplot as plt

rng = np.random.default_rng(seed = 42)

Sampling and Plotting#

NumPy provides a utility to generate pseudo-random numbers. We shall try to sample points from various distributions. Once we have a sample, we can then represent it pictorially using suitable plots.

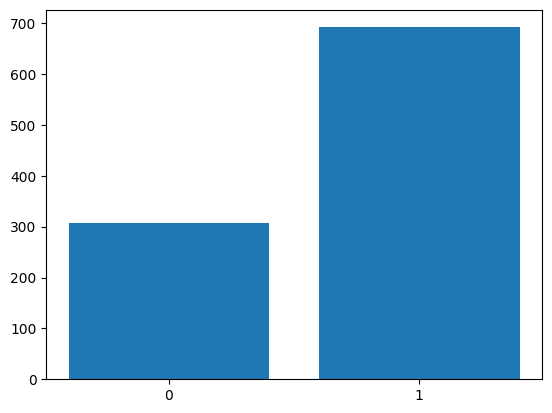

Sampling: Bernoulli#

Let us generate a sample of \(1000\) points from the \(\text{Br}(0.7)\).

In NumPy:

X = rng.choice([0, 1], p = [0.3, 0.7], size = 1000)

X.shape

(1000,)

Plotting: Bar plot#

Let us visualise the sample using a bar plot. For this, we first need the height of the bars.

zero, one = 0, 0

for i in range(X.shape[0]):

if X[i] == 0:

zero += 1

else:

one += 1

There is a better way of getting the height of the bars. We will learn this when we study advanced indexing.

plt.bar([0, 1], [zero, one])

plt.xticks([0, 1]);

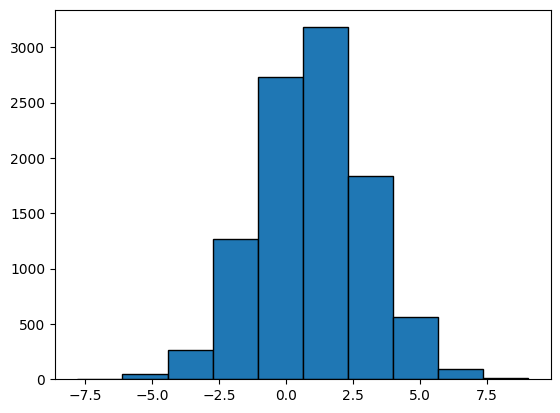

Sampling: Gaussian#

We now generate a sample of \(10,000\) points from \(\mathcal{N}(1, 4)\). Recall that \(\mu = 1\) and \(\sigma^2 = 4\).

X = rng.normal(1, 2, size = 10_000)

X.shape

(10000,)

Plotting: Histogram#

We can now visualise the sample using a histogram.

plt.hist(X, bins = 10, edgecolor = 'black');

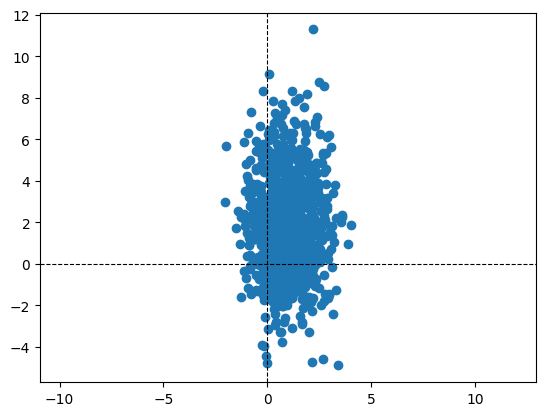

Sampling: Bivariate Gaussian#

Sample 1000 points from the following Bivariate Gaussian:

mu = np.array([1, 2])

cov = np.array([

[1, 0],

[0, 5]

])

X = rng.multivariate_normal(mu, cov, size = 1000).T

# we transpose so that the data-matrix is (d, n) and not (n, d)

d, n = X.shape

Plotting: Scatter plot#

Let us now visualise the sample using a scatter plot. Zooming out of the scatter plot gives us a better understanding. Changing the covariance matrix also helps in understanding how the sampled points depend on it.

plt.scatter(X[0], X[1])

plt.axis('equal')

plt.axhline(color = 'black', linestyle = '--', linewidth = '0.8')

plt.axvline(color = 'black', linestyle = '--', linewidth = '0.8')

<matplotlib.lines.Line2D at 0x7fb6825d30d0>

Estimating the sample covariance matrix#

Let us now estimate the sample covariance matrix and verify if it is close to the population covariance matrix. For this, we use extend the concept of a norm to matrices.

d, n = X.shape

mu = X.mean(axis = 1).reshape(d, 1)

C = (X - mu) @ (X - mu).T / n

C

array([[ 0.93985785, -0.03385001],

[-0.03385001, 5.12296728]])

# Check how close C and cov are

np.linalg.norm(C - cov)

0.1450161250795069

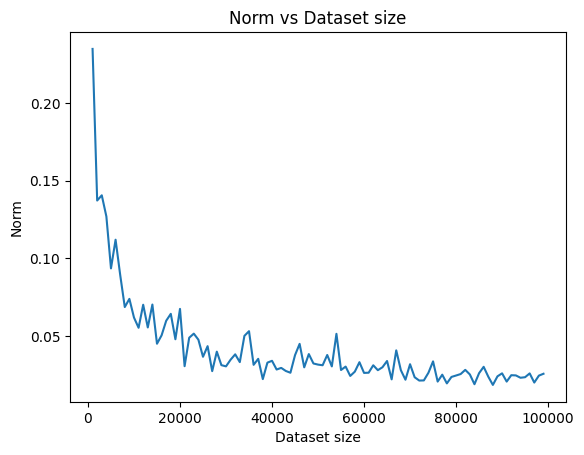

Study: Sample covariance vs Population covariance#

As an exercise, let us vary the number of data-points and notice the effect it has on the value of the norm computed above. We expect the norm to be smaller as the dataset’s size increases. We perform the following steps:

A function that generates the dataset for a given size.

A function that uses the generated dataset to compute thee sample covariance matrix.

def generate(mu, cov, n):

X = rng.multivariate_normal(mu, cov, size = n).T

return X

def sample_covariance(X):

d, n = X.shape

mu = X.mean(axis = 1).reshape(d, 1)

X -= mu

return X @ X.T / n

We now run this for different values of the dataset size, \(n\). For each \(n\), we run the experiment \(T\) times and then average the norm. We then plot the norm versus the value of \(n\)

mu = np.array([1, 2])

# population covariance matrix

cov = np.array([

[1, 0],

[0, 5]

])

# Run experiment

T = 10 # number of runs for each n

norms = [ ]

n_vals = np.arange(1000, 100_000, 1000)

for n in n_vals:

norm = 0

for t in range(T):

X = generate(mu, cov, n)

C = sample_covariance(X)

norm += np.linalg.norm(C - cov)

norms.append(norm / T)

# Plot

plt.plot(n_vals, norms)

plt.title('Norm vs Dataset size')

plt.xlabel('Dataset size')

plt.ylabel('Norm');

We see how the norm keeps going down as the dataset’s size keeps growing. This confirms our belief that the sample covariance matrix becomes a more accurate estimate of the population covariance matrix as the dataset’s size increases.

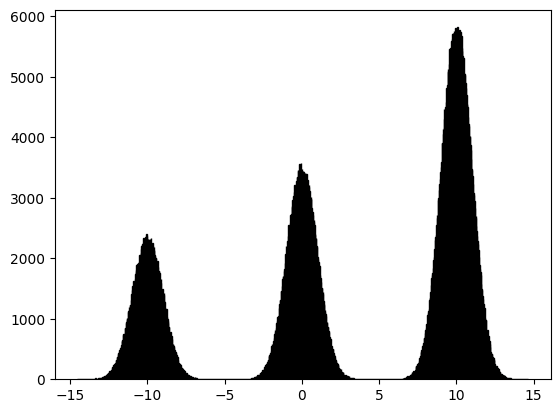

GMM#

Let us now draw \(1,000,000\) samples from a Gaussian Mixture Model (GMM) that has three components, with mixture probabilities \([0.2, 0.3, 0.5]\) and means \([0, 5, 10]\). The standard deviation of all three Gaussians is the same and is equal to \(1\). We can visualise the sample using a histogram.

n = 1_000_000

comp = rng.choice([0, 1, 2], p = [0.2, 0.3, 0.5], size = n)

mu = np.array([-10, 0, 10])

X = np.zeros(n)

for i in range(n):

X[i] = rng.normal(mu[comp[i]], 1)

plt.hist(X, bins = 1000, edgecolor = 'black');